Why you should start saving for a home now

Here’s a topic that everyone is currently talking about: inflation and the rising cost of living. Covid-related supply problems and the war in Ukraine are the immediate causes. Food, fuel and energy prices have been increasing at rates not seen for more than a decade. In these times, it is understandable that for many of you, stashing money away becomes all the more difficult. This includes saving for your first home. But that you must start (or continue) should be a top priority. Even if you’re young and not yet ready to buy a property, you should start saving for a house as early as possible.

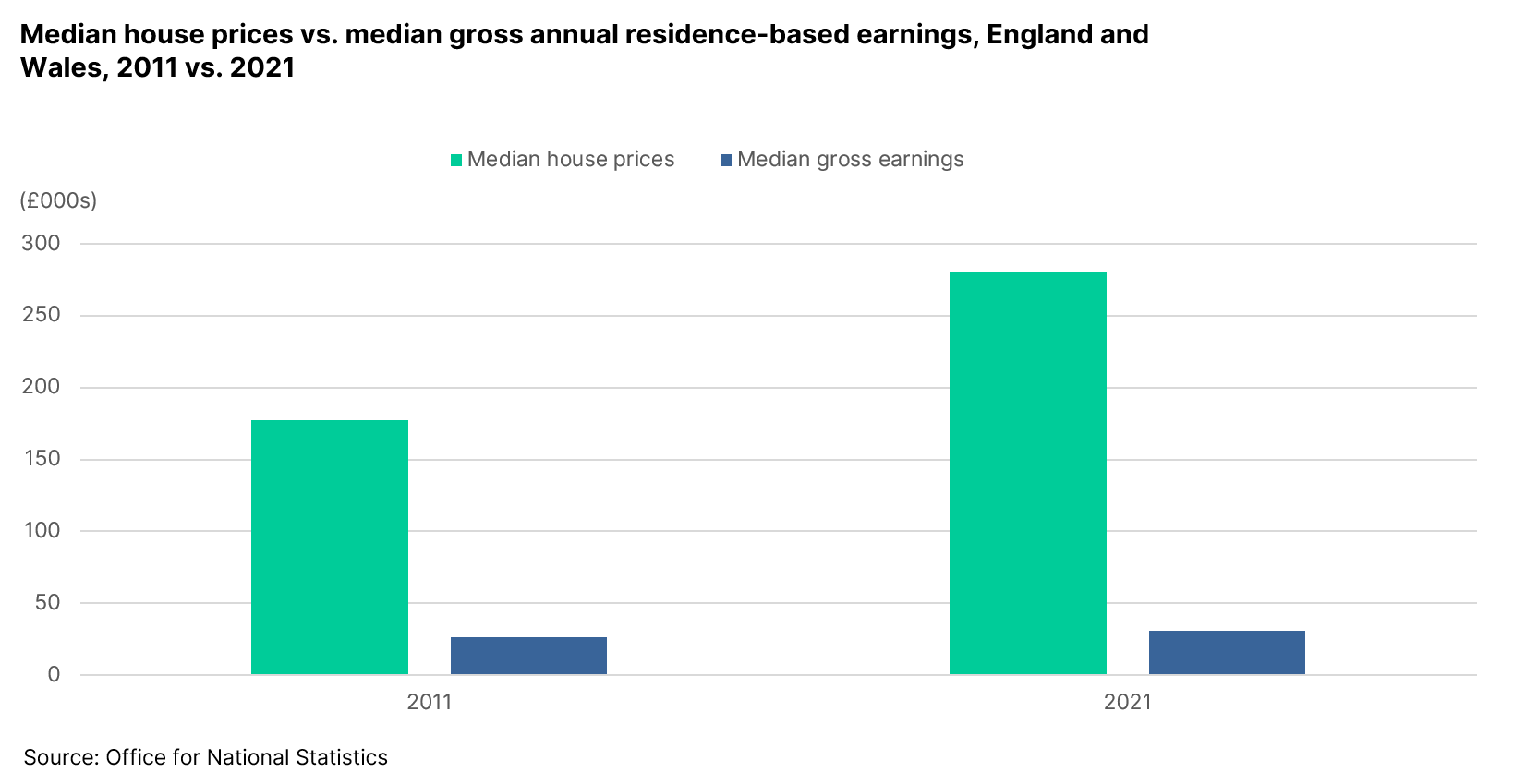

For several years now, house prices have risen at a faster pace than earnings, and housing affordability has worsened across all regions in the country, not just in London and the South East. House prices in relation to earnings are at record levels, and just in England, the median house price to median earnings multiple hit over 9.0 in 2021 compared to 6.8 a decade ago. This means you will need to save more money for your house deposit than ever.

Buying a home requires a habit for saving

With such challenging house affordability levels, getting on the housing ladder will not be easy. Setting money aside should be a discipline that you cultivate early. Typically, you were once financially dependent on your parents. After you graduated from university, moved out of your family home, and started developing your career, your choices and spending decisions have a major impact over time on your personal finances. A September 2020 research study by Aviva found that a silver-lining of the Covid lockdowns was that “nearly two-thirds of people have become more of a saver”. By eating out less, taking fewer holidays and spending less on personal goods, people have handsomely boosted their savings. For many, the habit has stuck and they have vowed to maintain such new saving habits. Aviva predicts that 28% of people aged 25-34 are likely to maintain these saving habits. This can be the holy grail to you buying your first dream home.

Say you begin saving at the age of 24 and put away £300 consistently each month over the next 6 years. By the time you’re 30, you’ll have saved a pot worth £21,600. With a 10% home deposit, you could afford a property worth £216,000. This can be higher if you can muster any additional savings, investments and contributions from Bank of Mum and Dad (BOMAD).

Putting down a larger home deposit is more advantageous

When you have saved enough and are ready to buy your home, you’ll approach lenders for a mortgage. The most important thing that affects what price you can afford for a house is how much you can borrow. And how much you can borrow is determined by the lender, principally from your earnings and your deposit. They apply rules based on Loan to Income (LTI) and Loan to Value (LTV) ratios. The government launched the much-publicised Mortgage Guarantee Scheme in April 2021, where lenders can lend up to 95% of the value of a property. However, as enticing as it may sound, if you have only a 5% deposit, net of stamp duty and other home-buying fees, the lender will charge you a risk premium with a higher interest rate. This couldn’t have been put more clearly than in the words of money saving expert, Martin Lewis who advised: “bear in mind that rates tend to be MUCH higher if you’ve got less than 10% deposit, so if you can push for a 10% deposit then you’ll get access to a cheaper mortgage”. In short, save early and save enough for a minimum 10% deposit.

Saving money early can result in extra investment gains

If you are convinced, then start saving for your house early and give yourself a few years before your home purchase. If you are in a relationship, then convince your partner to do the same. Starting early allows you to benefit from gains on your savings over time through the power of compounding. It can be understood as ”adding interest on interest” and can create a snowball effect on your savings.

There are multiple ways you can realise these gains. For example, you can open a tax-free ISA account and if appropriate, a Lifetime ISA (LISA) account that would be boosted by free government cash of up to 25%. You can also invest your savings in fixed deposits and low-cost stocks and shares portfolios that are suitable for your situation, especially your time horizon. With stock & shares, you could experience gains from dividend income compounding. The key factors in making it work in your favour are time and consistent saving behaviour. Do it right and you have now embarked on the right path to one day soon owning your dream home.

The bottom line

The current climate should be a catalyst for you to start saving for a house now. Ideally, you want to give yourself time to cultivate good savings habits, save up enough for a home deposit and experience those gains on your savings. If you’re thinking about getting your own home one day, check out Habstash to see types of homes in your desired area that are closest to your affordability.

DISCLAIMER: The content on our site is provided for general information purposes only and is not intended to amount to advice on which you should rely. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.